Global stock markets currently hover around all-time highs, last year’s performance was tremendously good, and interest rates are back. No wonder that the media and market strategists recently began to spread an old narrative – the idea of Cash on the Sidelines.

Every time someone says, “There is a lot of cash on the sidelines,” a tiny part of my soul dies.

Cliff Asness – 2014 – My Top 10 Peeves – Page 25

Since this post appears in my Standard Stupidities category, you already now its direction… Spoiler: the most fundamental feature of markets and a little thinking effort easily destroys the narrative as it is commonly used. But let’s go through it step-by-step…

- The Narrative of Sidelines

- The Problem of Sidelines

- Perspectives Matter

- Investor-Specific Sidelines

- The Psychology of Sidelines

The Narrative of Sidelines

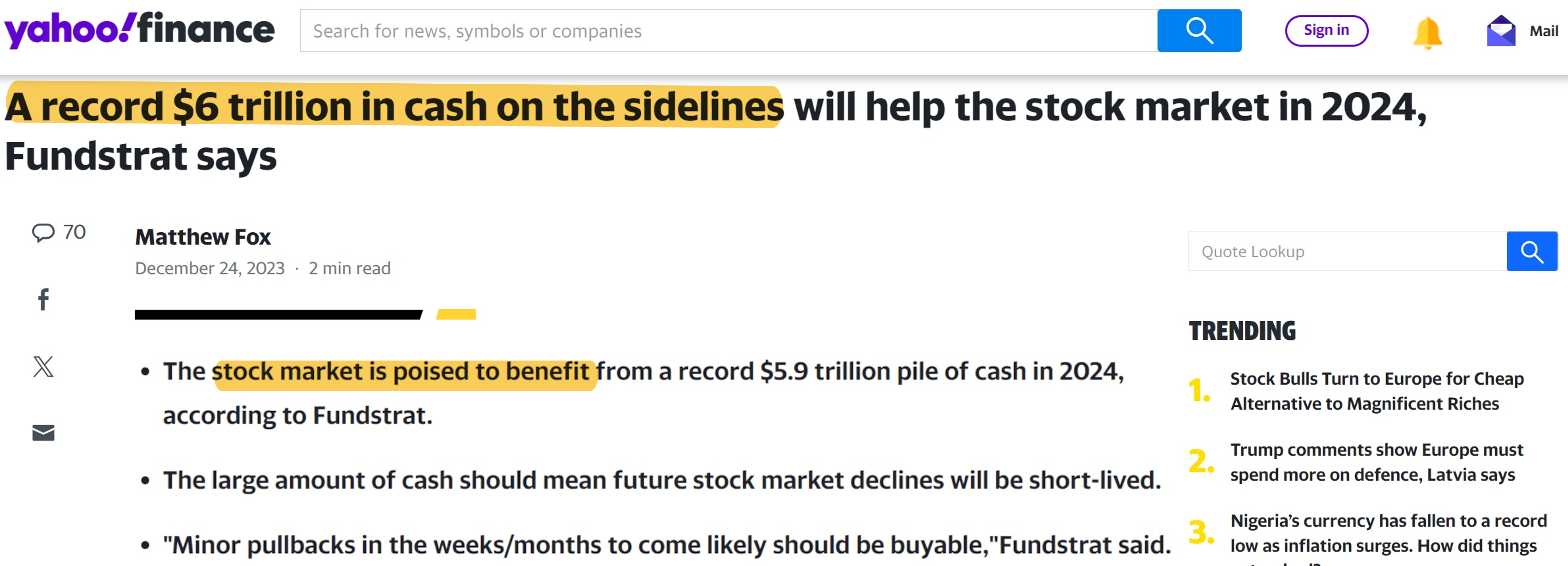

Before we explore why our souls should be dying when listening to Cash on the Sidelines debates, let’s start with an example. As in any battle, the first step to beat your enemy is to know what it looks like. Therefore, I screenshotted the following article from December 24, 2023 as a representative example for the narrative.

At least how I see it, the article clearly intends to express a positive opinion for stock markets in 2024.1Full credit, as of February 27, 2024, this was completely right. The author quotes a fund strategist who explains that investors currently hold about $6 trillion in money market funds. Even more important, he argues that this capital will act as sort of a backstop for equity markets or push prices even higher. At first glance, this seems very intuitive. New money flows into the stock market, so aggregate market capitalization and prices will rise. Or the other way around, there are enough potential buyers who will support the market when prices fall from the current highs.

The narrative of course also works in reverse. Strategists and the media often use it as negative indicator when investors exit the stock market and pile-up Cash on the Sidelines. The apparently intuitive mechanism is exactly the same. Money flows out of the stock market, so aggregate market capitalization and prices will fall.

Another component of the narrative are investors’ implied expectations. A lot of Cash on the Sidelines, according to some proponents of the narrative, suggests that investors are reluctant to invest in stocks (or any risky asset) and could indicate negative sentiment. Similarly, according to this logic, very little Cash on the Sidelines could indicate positive sentiment. We will see below that under some assumptions, this is the least wrong and in some cases maybe even useful aspect of the narrative.

The Problem of Sidelines

Getting back to the $6 trillion Cash on the Sidelines in the article above. Let’s go through a thought experiment to identify the problem with the narrative. Suppose the investors indeed deploy their cash and buy stocks. How does this work? Well, they go to the market and buy shares. But shares don’t fall from heaven. If I want to buy an Apple share, there is no magic force that creates it for me. I can only buy it from someone who sells it to me. So in order to deploy $6 trillion of Cash on the Sidelines, someone else must sell shares that are worth exactly – what a coincidence – $6 trillion.

Transactions can neither create nor destroy cash or securities. They just redistribute them among investors. So in our example above, we again end up with $6 trillion of Cash on the Sidelines, just with different owners. Obviously, stock prices can change in this process. We will come to that later.

In general, however, the Cash on the Sidelines narrative violates one of the most fundamental principles of markets: every buyer needs a seller and vice versa. Whenever you buy or sell a security (or any other product or service), there is someone on the other side who does the exact opposite transaction. Otherwise there would be no market. So in aggregate, there are no sidelines and there is no Cash on the Sidelines. There is just cash. The narrative that the market must increase when investors deploy $6 trillion is therefore flawed.

But what about the price impact of such transactions? Well, this one is actually quite difficult to answer. Transactions can neither create nor destroy cash or securities, but transacting parties can of course negotiate a higher or lower price. For example, suppose investors want to deploy their $6 trillion and face sellers who don’t want to sell at the current price. In this case, prices must actually increase to bring buyers and sellers together. But this is by no means certain. We could similarly make the example that sellers are desperately waiting for buyers and are willing to sell at the current price or even below that.

Bottom line: the pure fact that there are $6 trillion of Cash on the Sidelines in money market funds is by itself neither positive nor negative for the stock market. It is just a fact. We don’t know if the money market investors are actually willing to deploy this cash. Even if, we also don’t know the price at which existing investors would be willing to sell. The narrative that Cash on the Sidelines automatically supports stock markets is therefore flawed. It may be a catchy headline, but it violates some fundamental principles of markets and we simply don’t know its impact on prices.

Perspectives Matter

If you want to criticize my arguments above, you can of course make up a situation where it is actually possible that investors enter the stock market without others exiting. The most evident examples are Initial Public Offerings (IPOs), Seasoned Equity Offerings (SEOs), or de-listings. Suppose for (a very hypothetical) example, that the $6 trillion flow into the stock market via a series of IPOs that are exactly worth $6 trillion. In this case, aggregate market capitalization would indeed increase by $6 trillion and the money market funds are “empty” thereafter.

Two things to consider. First, higher aggregate market capitalization doesn’t necessarily translate into a higher price per share. Second, the fundamental principles and mechanisms of markets don’t change. You cannot buy an IPO without someone on the other side – every buyer still needs a seller.

This raises a very important point, however. Sidelines are all about perspective. Let me digress for a moment. The underlying equilibrium-thinking that I used to argue against sidelines originally comes from Physics. Most prominently, there is something called the Law of Conservation of Energy which says that the amount of energy in a defined system doesn’t change. Energy can only change its forms, but you cannot destroy or crate energy out of nowhere.

As I mentioned, the same is true for cash and securities. At least over the short-term, the amount of cash and wealth in our world are fixed.2Of course, central banks can and do adjust the amount of money over longer time horizons. This is something to analyze separately. We cannot destroy or create stocks with transactions. The key point, however, is how you define the world or the system you are looking at. In aggregate, there are and will be no sidelines. But for smaller sub-systems, there can be.

Back to the example with the IPO. We need to broaden our perspective to debunk the sideline narrative in this case. It is true that no existing investor must sell when new investors buy $6 trillion worth of IPOs. But this is just the perspective of the stock market. Someone outside this sub-system must still pile up Cash on the Sidelines of – you guessed it – exactly $6 trillion. Who are the sideline-creating counterparties in this case? Well, whoever sells the company in the IPO. Most likely, these are private equity companies, the founders of the business, or any other private owners. Once we include those in our definition of the system, there are again no sidelines and the cash just changes its owners.

Since we already discuss the role of perspective, let me briefly mention two other sideline-related narratives. The destruction of wealth from bankruptcies or strong stock declines when firms miss their earnings forecast or publish whatever other negative result.

The second one should be easy by now. Transactions can neither destroy nor create wealth or market capitalization. They just exchange cash for stocks and adjust prices. In aggregate, everything cancels out. The losses of the selling investors exactly balance the lower amount of cash required for the buying investors to enter their positions.

Bankruptcies are somewhat more difficult. People have the impression that bankruptcies are the only lose-lose situations in capitalism. But is this really true? Let’s make an example. Suppose we start a company and finance it with $500m equity and a one-year $500m loan. The business model is terrible, we as founders are incompetent, and our company doesn’t make a sale in its first year.3This may sound obskure and is certainly exaggerated, but some start-ups in industries like Biotechnology actually operate without sales in their first years. Hopefully with good business models and competent management, though. However, we had costs of $700m for whatever stuff and paid those in cash. So at the end of the first year, we have a loss of $700m that wipes out the entire equity and our company is bankrupt. There are only $300m left which is insufficient to repay the $500m loan. What will happen? Well, the lenders get the remaining $300m and record a loss of $200m. The equity investors receive nothing and record a loss of $500m. Overall, the company destroyed $700m in value. Really?

From the perspective of the debt and equity investors of this single company, this is of course true. But in aggregate it is not. As long as we didn’t withdrew the $700m in dollar bills and destroyed them, the cash must be somewhere. And of course, the costs of our company are the revenues of another company. So if we spent the $700m for a company yacht and a private jet, the yacht and jet company are effectively the other side of our bankruptcy. Once again, the cash just changed its owners but didn’t disappear.

Bottom line: in aggregate, there are and will be no sidelines. At least over the short-term, the amount of cash and wealth is fixed and transactions can only re-distribute it. Whenever you find yourself in a situation where cash or wealth seems to be destroyed or created, you either deal with the central bank or should probably broaden your perspective to find the counterparty.

Investor-Specific Sidelines

Since it is all a matter of perspective, we can use this to our advantage and analyze the cash holdings of single investors or investor groups. With a severe lack of imagination for cool names, I call those Investor-Specific Sidelines.

For example, the annual report from Warren Buffett’s Berkshire Hathaway just came out at the time of writing this. Per end of 2023, Berkshire held about $163.3b in cash, cash equivalents, and short-term treasury bills. At the current market cap of about $900b this is a cash ratio of roughly 18%. While Berkshire’s cash position depends on much more than just its investment outlook, you could still argue that such a high cash ratio is a somewhat negative indicator. In fact, Warren Buffett communicates quite clearly that there are almost no attractive investment opportunities that are large enough to move the needle for his giant portfolio. From that, some people infer that US large caps are too expensively valued right now.

Before the Cash on the Sidelines fans celebrate, note that we are doing something completely different here. Like everyone else, Warren Buffett needs a counterparty to purchase stocks. So when he enters the market, someone else must exit. By using his cash ratio as an indicator we assume that he is smarter than his counterparty. This is an entirely different question than what will happen to prices when his $163.3b flow into the market.

Of course, Buffett is a very prominent example for such an analysis. However, we can apply this idea to virtually every supposedly smart investor or even to entire investor groups. For example, we could analyze the aggregate cash positions of retail investors, hedge funds, institutional investors, mutual funds or whatever else. I repeat myself, but all of those actors still need counterparties for their trades. Using their cash ratios as indicators therefore implicitly assumes that they are smarter than those who sold to them.

The Psychology of Sidelines

As with any Standard Stupidity, we can finally ask where it comes from and why it is so hard to stop. Before we continue, a few disclaimers for this remaining paragraph. Everything that follows are loose ideas how certain concepts of psychology and behavioral economics relate to the Cash on the Sidelines narrative. It is not a thorough analysis and by no means comprehensive or complete.

The obvious first explanation are the incentives of the media and fund strategists. I don’t want to be too cynical, but it is financial reporters’ and strategists’ job to receive attention and/or animate investors to do something. A catchy headline, a supposedly intuitive mechanism, and a widespread narrative seems more helpful than abstract and boring general-equilibrium thinking in this respect.

That was the easy one. But why do our brains like the narrative so much? One explanation that came to me will thinking about it is Daniel Kahneman’s model of System 1 and 2. For the full explanation, I highly recommend his book Thinking, Fast and Slow, but let me give you the idea. Kahenman uses the metaphor of System 1 and 2 to explain two fundamentally different modes of our brain.

Daniel Kahneman – 2011 – Thinking, Fast and Slow – Chapter 1

- System 1 operates automatically and quickly, with little or no effort and no sense of voluntary control.

- System 2 allocates attention to the effortful mental activities that demand it, including complex computations. The operations of System 2 are often associated with the subjective experience of agency, choice, and concentration.

In English, System 1 is something like our autopilot and a very efficient way to solve simple and easy tasks. It is also responsible to execute our habits. In contrast, System 2 requires effort to activate and distinguishes us from many other animals as it allows to solve complex problems. Needless to say, both systems have their reasons for existence. However, we shouldn’t rely on System 1 to solve complicated problems and identify our weaknesses when we try to do so.4To be fair, we also shouldn’t waste energy to activate System 2 for a simple task that doesn’t require it.

I think this is a quite useful model to think about the Cash on the Sidelines narrative. Even though it is wrong, our System 1 clearly likes the apparently intuitive mechanism that outside cash supports the stock market. Activating our System 2 to think more deeply about what it means to “deploy sidelines” requires energy and effort.5From my own experience, I can tell you that it takes embarrassingly long to properly think through the concept to write about it in a blog post… Since yahoo finance estimates a reading time of 2 minutes for the article above, most people probably don’t even think about activating their System 2 to debunk the narrative and so it continues to make its way.

I don’t expect that this post will change anything at this situation. But for those who are willing to activate their System 2, I hope it is helpful. I also hope that you join the club of those with dying souls when listening to discussions about non-existing sidelines…

- StanStu #2: Missing the Best Days

- StanStu #1: Cash on the Sidelines

- Standard Stupidities: Introduction

This content is for educational and informational purposes only and no substitute for professional or financial advice. The use of any information on this website is solely on your own risk and I do not take responsibility or liability for any damages that may occur. The views expressed on this website are solely my own and do not necessarily reflect the views of any organisation I am associated with. Income- or benefit-generating links are marked with a star (*). All content that is not my intellectual property is marked as such. If you own the intellectual property displayed on this website and do not agree with my use of it, please send me an e-mail and I will remedy the situation immediately. Please also read the Disclaimer.

Endnotes

| 1 | Full credit, as of February 27, 2024, this was completely right. |

|---|---|

| 2 | Of course, central banks can and do adjust the amount of money over longer time horizons. This is something to analyze separately. |

| 3 | This may sound obskure and is certainly exaggerated, but some start-ups in industries like Biotechnology actually operate without sales in their first years. Hopefully with good business models and competent management, though. |

| 4 | To be fair, we also shouldn’t waste energy to activate System 2 for a simple task that doesn’t require it. |

| 5 | From my own experience, I can tell you that it takes embarrassingly long to properly think through the concept to write about it in a blog post… |